Destination Travel Trends

With the peak months of summer moving to the background, the attention of many turns more squarely towards winter. Shifts in school breaks are guaranteed to impact both pre- and post- Holiday periods, and consumers are tolerating rate better than 6 months ago, but not as well as last year.

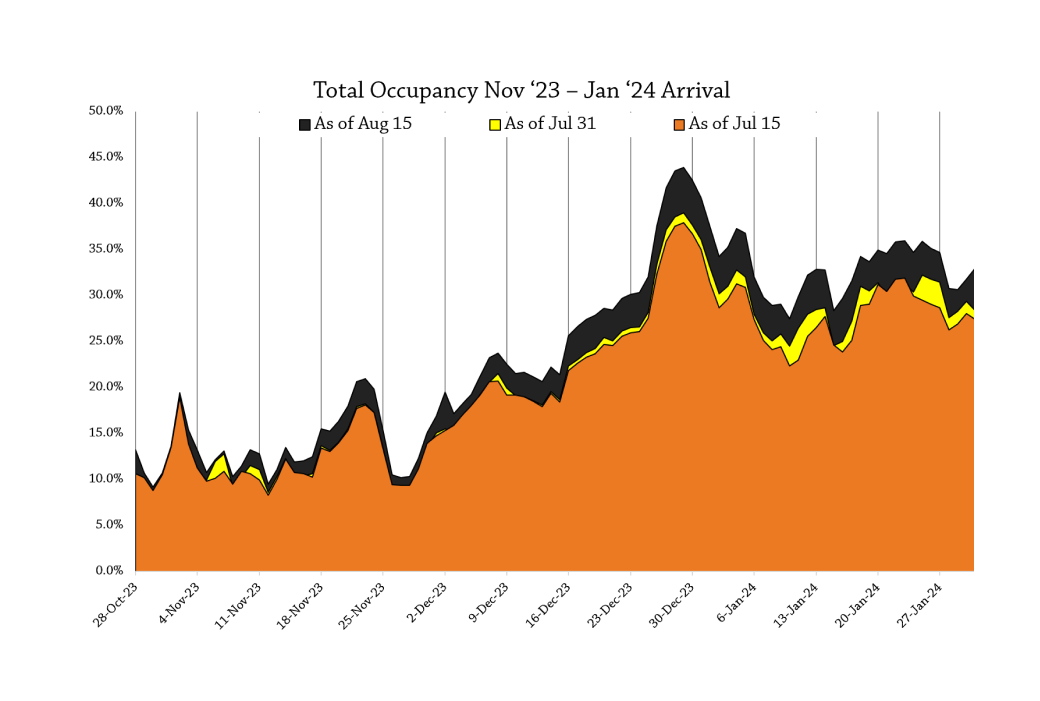

If we look at seasonal progression, it’s clear that a good foundation of bookings for winter has been established since mid-July (orange section on chart), and occupancy for December through January got a big boost in the first half of August (dark gray). But our attention is captured by what happened – or didn’t – with bookings in the last half of July for winter arrival. They’re conspicuous in their absence (yellow). The temporary dip in winter activity in late July is an outlier that’s not seen in any seasonal ramp-up going back to 2016 (pandemic excepted).

So, why did consumers put the brakes on winter bookings at a time when confidence surged, earnings outpaced inflation (again), Wall St approached records, and room rates were relaxing? The simple answer: “we don’t know”. While we have a wealth of excellent information at our fingertips, and almost always have clear, qualitative & quantitative explanations for how the market behaves, sometimes things just….. happen.

It’s a good reminder that no matter how hard you dig, sometimes you just need to be humble, shrug your shoulders, and move on……..