Trends

Based on Inntopia transactional data, average daily rate (ADR) for lodging transactions across destination travel markets is beginning to show some pattens. Some of the early ADR shock that followed the February 24 market freefall and then the cascade of events in early March have softened. ADR for bookings and rebookings being transacted April 15 for arrival dates up to the end of July is higher now than it was as of February 15. Though the gain is slight, this is an important reflection of survey results indicating a majority of lodging partners are resisting the urge to drop rates to the bottom of the market, which can lead to a long recovery. And while rates for later arrivals, August through November, are down overall from where they were as of February 15, the pace of decline for arrival in those months is slowing over time, suggesting lodging properties will continue attempting to hold rate if possible until the consumer is back with enough volume to indicate their rate tolerance.

Here are a few findings:

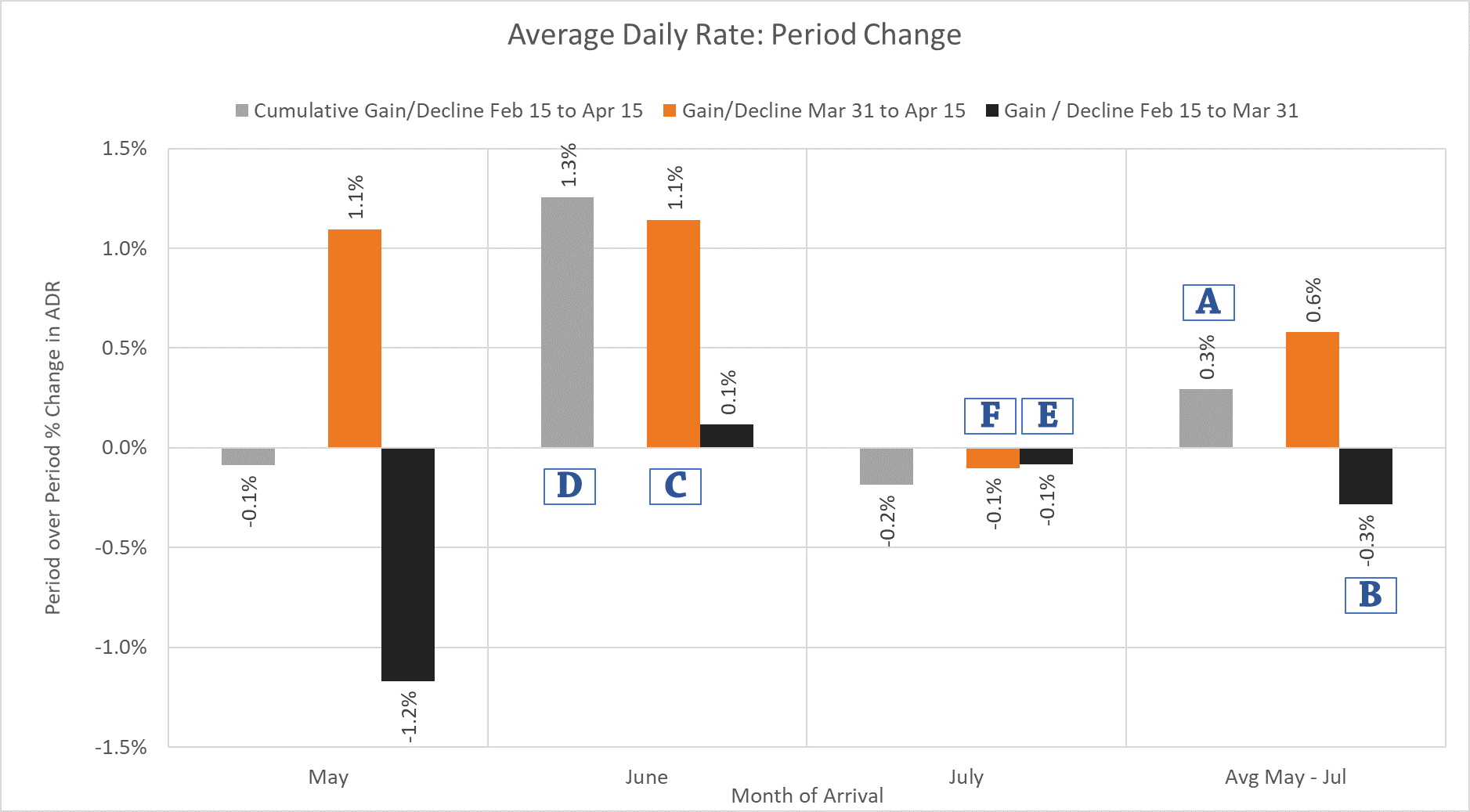

ADR for new bookings and rebookings as of April 15 arriving in May, June, and July is either above or all-but flat compared to where it was pre-crisis as of February 15. Overall, ADR for the three-month period is pacing up a cumulative 0.3% (“A” on chart) from where it was as of February 15, an improvement from the -0.3% decline as of March 31 (B). This is driven in large part in a strengthening of rate for bookings arriving in June, with ADR up 1.1% (C) compared to where it was as of March 31, and 1.3% (D) from where it was as of February 15. Bookings for arrival in July have seen very little change in their ADR between the three periods studied., with rate declining -0.1% between February 15 and March 31 (E), and an additional -0.1% between March 31 and April 15 (F).

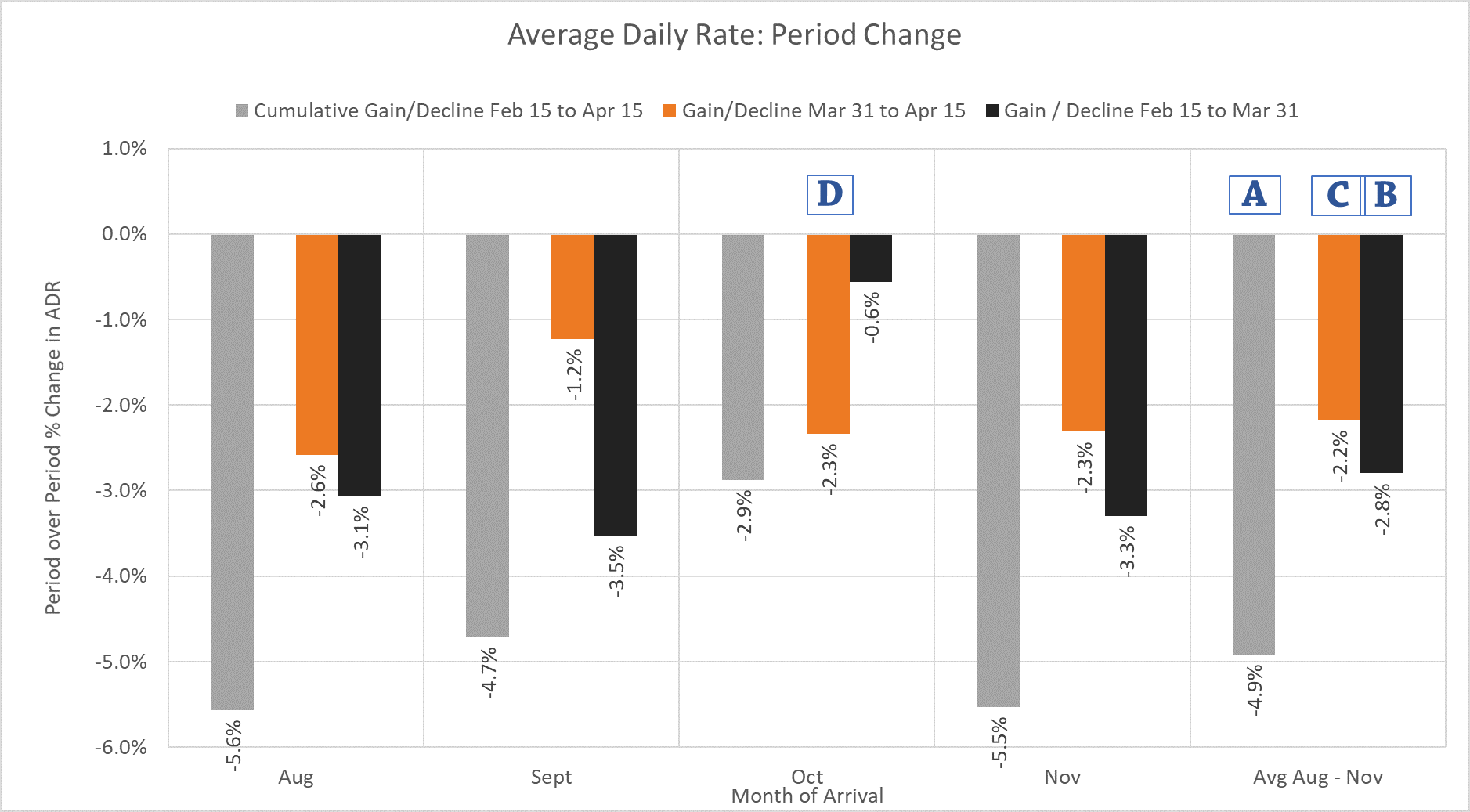

ADR for new bookings and rebookings as of April 15 and arriving in August, September, October, and November is down overall from where it was as of February 15, declining a cumulative average of -4.9% over that time (A). However, the pace of decline in ADR is slowing. Rates dropped an average of 2.8% between February 15 and March 31 (B), a pace that has slowed to -2.2% from March 31 to April 15 (C). Though the slowdown in decline is a positive development, consecutive declines can add up quickly and put the industry at-risk of a long rate and revenue recovery. An exception to the slowing pace of ADR decline in the longer lead reservations is bookings for arrival in October, where rate decline has intensified slightly from -0.6% between February 15 and March 31 to -2.3% between March 31 and April 15 (D).